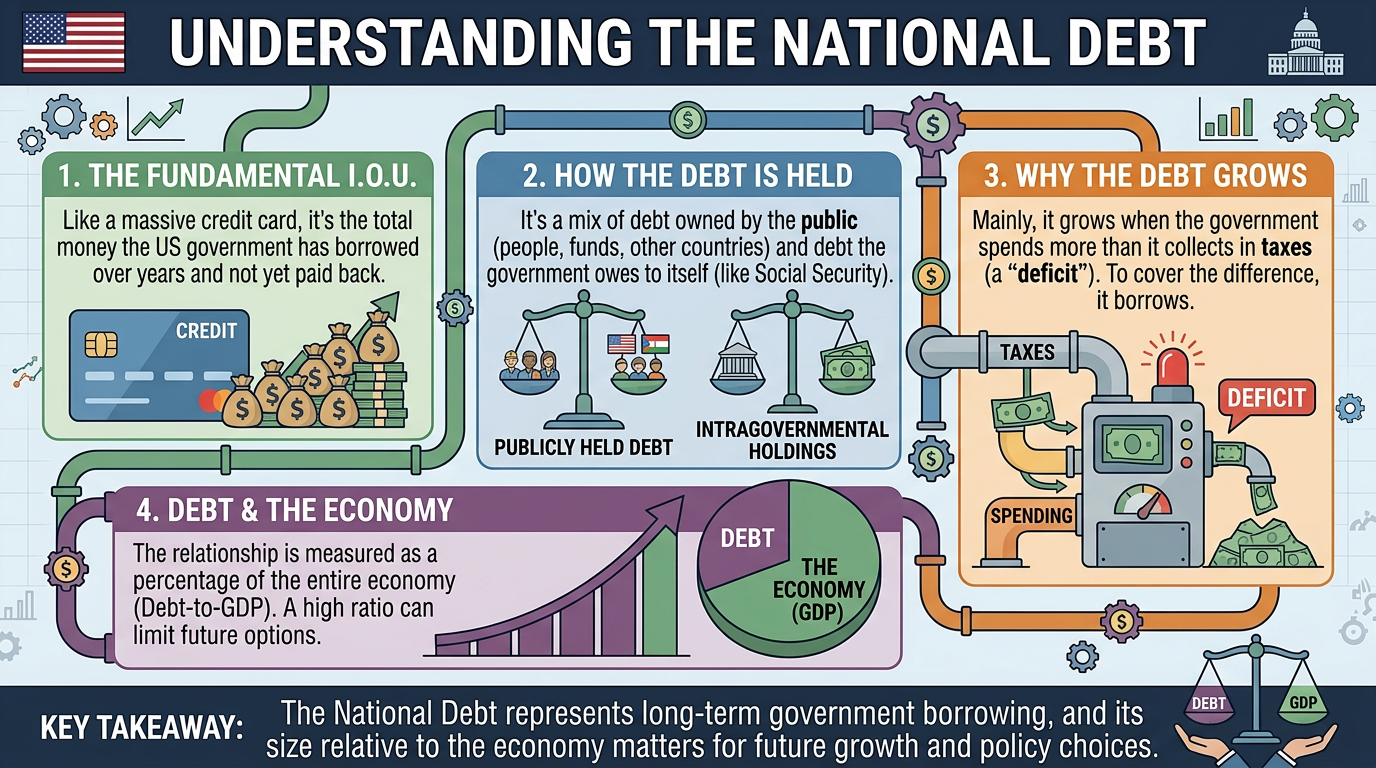

Unpacking the Trillions Behind the National Debt

Every time politicians debate the federal budget, the national debt takes center stage. You might hear staggering figures in the trillions of dollars, accompanied by warnings that the country is running out of money. Despite the alarming headlines, the national debt is rarely explained in plain English. Simply put, the national debt is the total amount of money the federal government has borrowed over its history to cover its expenses.

The Annual Tab Versus the Total Bill

The easiest way to understand the national debt is to compare it to how a person might use a credit card. Every year, the government collects money, mostly through taxes paid by citizens and businesses. This is its income. During that same year, the government spends money on things like military defense, national parks, and healthcare programs.

When the government spends more money in a single year than it collects in taxes, the leftover unpaid amount is called a deficit. To pay for that year's deficit, the government has to borrow cash. The national debt is simply the grand total of all those yearly deficits piled up over the entire history of the country.

How the Government Borrows Money

When you need to borrow money, you might go to a bank and apply for a loan. When the United States government needs to borrow money, it issues official IOUs. These government IOUs are usually called Treasury bonds.

When someone buys a government bond, they are handing their cash over to the government to spend today. In exchange, the government gives them a piece of paper (nowadays its a digital record) promising to pay that person back at a specific date in the future. As a reward for lending the money, the government also promises to pay a little extra on top of the original amount, which is the interest.

Who Actually Owns the Debt?

A common misconception is that the United States owes all of its massive debt to foreign countries. In reality, the picture is much more domestic. While foreign nations do buy American bonds, a huge portion of the debt is actually owed to the American people and American institutions.

If you have a retirement account, a pension plan, or money in a mutual fund, there is a very good chance your portfolio includes some government bonds. American banks, local state governments, and even the Federal Reserve hold massive amounts of this debt. In a very real way, a large chunk of the national debt is money the country owes to its own citizens.

The Ripple Effect of a Growing Tab

Borrowing money is not inherently bad; it allows the government to fund important national projects or respond to emergencies without instantly raising taxes on everyday people. However, carrying a massive debt does have real-world consequences.

Just like a person with a large credit card balance, the government has to make regular interest payments on the money it borrowed. As the debt grows larger, those interest payments eat up a bigger and bigger slice of the national budget. This means a larger portion of your tax dollars goes strictly toward paying off the interest from past borrowing, leaving less money available to spend on current needs like repairing roads, funding schools, or investing in new medical research. Furthermore, if the government needs to borrow massive amounts of money constantly, it competes with regular businesses trying to get loans, which can eventually drive up interest rates for everyone.

Summary

The national debt is the grand total of all the money the federal government has borrowed over time to cover the gap between what it collects in taxes and what it spends. By issuing government bonds, the country borrows cash from foreign nations, domestic banks, and everyday investors, promising to pay it back with interest later. While this borrowing allows the country to function and invest in its future during tough times, a continuously growing debt means a larger portion of taxpayer money must be used to pay off past interest rather than funding tomorrow's needs.