A Practical Guide to Buying and Selling Bonds

While many people understand the basic concept of lending money to an institution for a guaranteed return, the actual mechanics of purchasing a bond often remain a mystery. Unlike buying a share of stock, which is usually as simple as tapping a button on a smartphone app, the bond market operates through a few different channels depending on what exactly you want to buy.

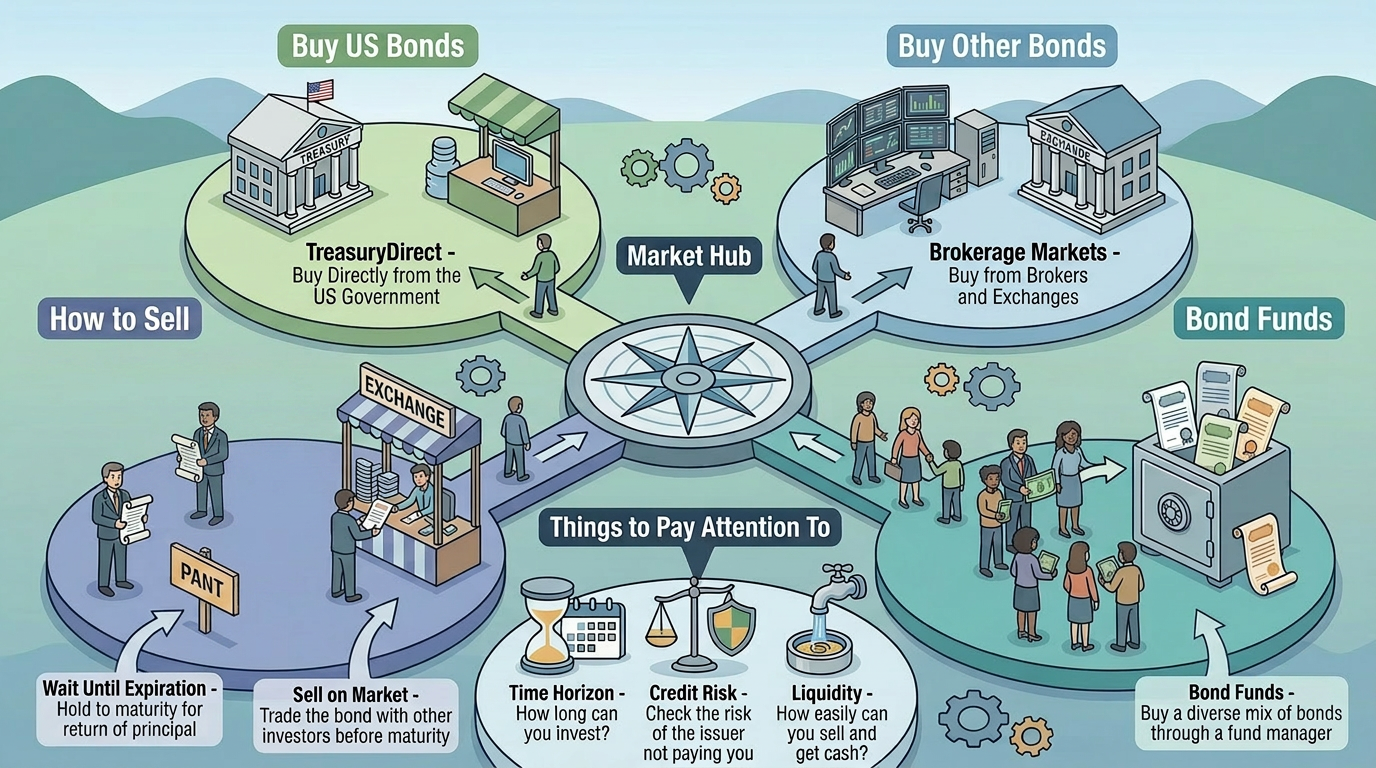

Going Straight to the Source for Government Debt

If you want to lend your money directly to the United States federal government, the process is surprisingly straightforward. The government runs its own official website, called TreasuryDirect, specifically for this purpose.

Through this online portal, everyday citizens can buy brand-new government bonds without needing a middleman or a financial advisor. You simply create an account, link your standard bank account, and choose which type of government loan you want to fund. Because the government wants to encourage everyday people to save, they make the barrier to entry very low. You can typically purchase these government bonds for as little as one hundred dollars. When you buy through this direct route, the government simply deposits your interest payments, and eventually your original cash, straight back into your linked bank account.

Navigating the Brokerage Market

If you want to buy bonds from a city government, a massive corporation, or if you want to buy older, existing bonds from other investors, you will need to use a standard brokerage account. This is the same type of account you would open with major financial companies like Fidelity, Charles Schwab, or Vanguard to buy regular stocks.

Inside your brokerage account, there is a dedicated section for trading bonds. Here, you can search through thousands of available loans. You can filter them by who is borrowing the money, how long the loan lasts, and how much interest they are paying. However, purchasing individual bonds this way usually requires a much larger budget. In the standard brokerage market, individual bonds are typically sold in increments of one thousand dollars, meaning you cannot just buy fifty dollars' worth of a corporate loan.

The Shortcut of Bond Funds

For many beginners, trying to pick a single, individual bond to buy can feel overwhelming. To solve this, the financial industry created bond funds.

A bond fund is essentially a massive basket of different bonds grouped together. When you buy into the fund, you are buying a tiny slice of that entire basket. This is often the most popular route for everyday investors because it trades exactly like a regular stock. You can log into a basic investing app, search for a bond fund, and buy a share of it for a very low price. This instantly spreads your money out over hundreds of different government and corporate loans, completely removing the stress of picking just one. However, it is important to keep in mind that this convenience comes at a slight cost. The companies that manage these massive baskets charge a small, ongoing fee to do the work for you, which is taken out of your investment each year.

How Selling Actually Works

When it comes to getting your money out of the bond market, you have two distinct choices. The easiest choice is to do absolutely nothing. If you hold onto an individual bond until its final end date, known as maturity, the borrowing organization simply deposits your original cash back into your account, and the transaction is permanently closed.

Your second choice is to sell the bond early. If you bought an individual bond through a brokerage, you can list it for sale on their open marketplace. As discussed previously, the price you get will depend heavily on current national interest rates. If you need to sell your bond on a Tuesday, and national interest rates happen to be very high that week, you might have to sell your bond to another investor for slightly less than you originally paid for it. If you opted for the easier route of a bond fund, you simply click the "sell" button on your app during regular market hours, and the cash is immediately returned to your account based on the fund's value that day.

Crucial Pitfalls to Watch Out For

Before you purchase any bond, there are a few important risk factors you must evaluate to protect your money:

The Borrower's Report Card: Just like a bank checks your credit score before giving you a mortgage, professional rating agencies grade corporations and cities on their financial health. A high grade (like "AAA") means the borrower is extremely safe and almost guaranteed to pay you back. A low grade (often called "junk") means the company is struggling. They will offer you a very high interest rate to tempt you, but there is a real risk they could go bankrupt and never return your money.

The Lock-Up Commitment: You must pay close attention to the timeframe of the loan. If you buy a twenty-year bond, you are locking your cash into that specific interest rate for two decades. If you think you might need that cash to buy a house or pay for college in three years, you should only look for short-term bonds to avoid the hassle and potential loss of trying to sell it early on the open market.

Finding a Buyer: If you decide to buy a bond from a very small, obscure town, you might find it difficult to sell if you need your money back early. Unlike stocks of major companies, which have millions of buyers waiting every second, highly specific bonds sometimes sit on the marketplace for a while before another investor decides they want to purchase them.

Summary

Buying and selling bonds requires a slightly different toolkit than navigating the stock market. For federal government loans, the direct Treasury website offers a simple, low-cost path. For corporate or city loans, a standard brokerage account gives you access to a massive inventory, though often at a higher price point. For those who want the easiest experience, bond funds offer a way to invest in a diverse basket of loans with the click of a button. By checking the financial health of the borrower and understanding the timeframe of the loan, you can safely navigate these marketplaces and add a reliable stream of interest to your financial portfolio.