A Practical Guide to the Different Types of Emergency Funds

An emergency fund is a stash of money set aside specifically to cover unexpected financial surprises. While the general concept is simple (saving for a rainy day), not all emergency funds are created equal. Depending on your career stability, lifestyle, and financial goals, the way you structure your safety net can vary significantly.

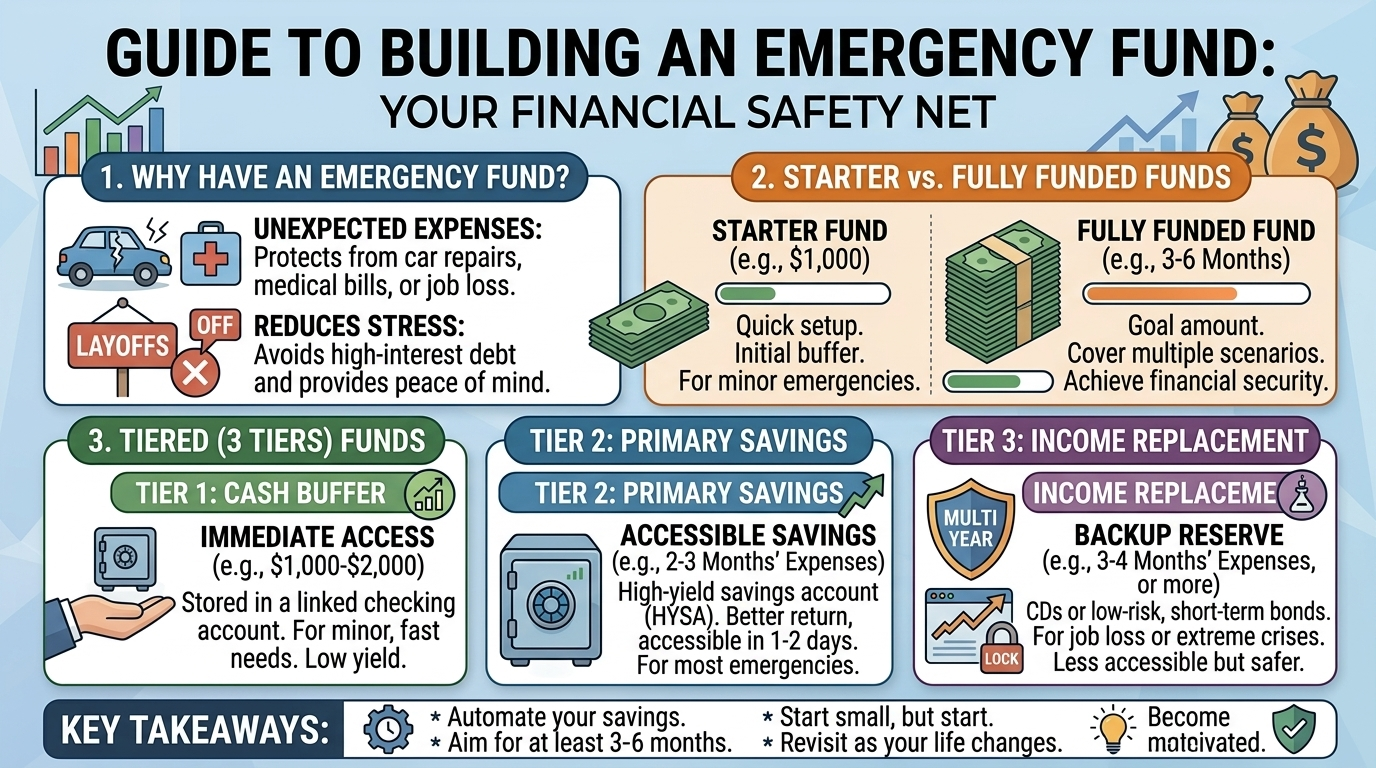

Starter Emergency Fund vs. Fully Funded Emergency Fund

To determine your target amount, calculate a single month of essential expenses by totaling your non-negotiable costs like housing, utilities, basic groceries, and debt minimums (things like mortgages & credit cards) while excluding luxury spending. You then multiply this baseline by your desired number of months to establish a clear savings goal that ensures you can cover your core needs during a crisis.

The first step in financial planning is often distinguishing between a temporary cushion and a permanent shield. A starter emergency fund is a small, initial goal, usually between $1,000 and one month of expenses. The purpose of this fund is to keep you from using credit cards or taking out loans when minor mishaps occur, such as a flat tire, a broken appliance, or a sudden trip to the vet. It is designed to be built quickly so you can focus on other financial goals, like paying off high-interest debt.

A fully funded emergency fund is the ultimate goal for long-term stability. This typically covers 3 to 6 months of essential living expenses. This fund is designed to protect you against major life disruptions, such as a job loss or a significant medical emergency. While it takes longer to build, it provides a level of security that allows you to navigate months of uncertainty without financial ruin.

High-Yield Savings vs. Cash Equivalents

Where you keep your emergency fund is just as important as how much is in it. The goal is to balance liquidity, which is how fast you can get the cash, with preservation, which means making sure the money does not lose value. High-Yield Savings Accounts (HYSAs) are the most common homes for emergency funds. They offer significantly higher interest rates than traditional savings accounts while keeping your money accessible. They are FDIC-insured, meaning your money is safe up to $250,000. Money Market Accounts (MMAs) are similar to HYSAs and often come with check-writing abilities or a debit card, making them slightly more liquid if you need to pay for a repair on the spot.

Another choice is to keep all your money in cash. While keeping a small amount of physical cash, perhaps $200 to $500, at home is useful for power outages or local emergencies, keeping a full emergency fund in physical cash is risky due to theft, fire, and inflation. In most cases, money market accounts or savings accounts are the best way to store money without worry.

The Job Stability Variable: 3 Months vs. 6 Months vs. 12 Months

The size of your emergency fund should match your personal risk profile because not everyone needs the same amount of money in their emergency fund. Three months of expenses is generally sufficient for individuals with high job security (relatively stable jobs), low housing costs like renters, or those who are single with few financial dependents. If you could find a new job within weeks, a smaller fund is often acceptable.

Six months of expenses is the standard recommendation for most households, especially those with children, mortgages, or those working in moderately stable industries. An extended fund of twelve months is recommended for freelancers, business owners, or people working on commission. If your income is unpredictable or if you work in a highly specialized field where finding a new role could take a year, a larger safety net is a necessity.

Tiered Emergency Funds

A sophisticated way to manage a safety net is through tiering. This strategy allows you to keep some money immediately available while letting the rest of your fund work a bit harder for you. Tier one is immediate and consists of $1,000 to one month of expenses in a standard checking or savings account for instant access.

Tier two is the core and holds the bulk of your 3 to 6 month fund in a High-Yield Savings Account. It takes 1 to 3 days to transfer to your checking account, which is fine for most big emergencies. Tier three is the extended portion for those who want a 12-month cushion. These extra months might be kept in slightly less flexible but still very safe options like CDs or bonds/treasuries. These accounts offer better protection against the rising cost of living, but they often require you to leave the money untouched for a set period or pay a small fee if you need to take it out early.

Summary

An emergency fund is not an investment; it is an insurance policy. While it might be tempting to put that money into the stock market to chase higher returns, the goal of an emergency fund is to be there when the market is down and your income is at risk. By starting with a small goal, choosing the right high-yield account, and scaling the fund to match your career stability, you create a foundation that allows the rest of your financial life to thrive without fear.