Market Summary March 30 - April 3, 2026

Market Summary

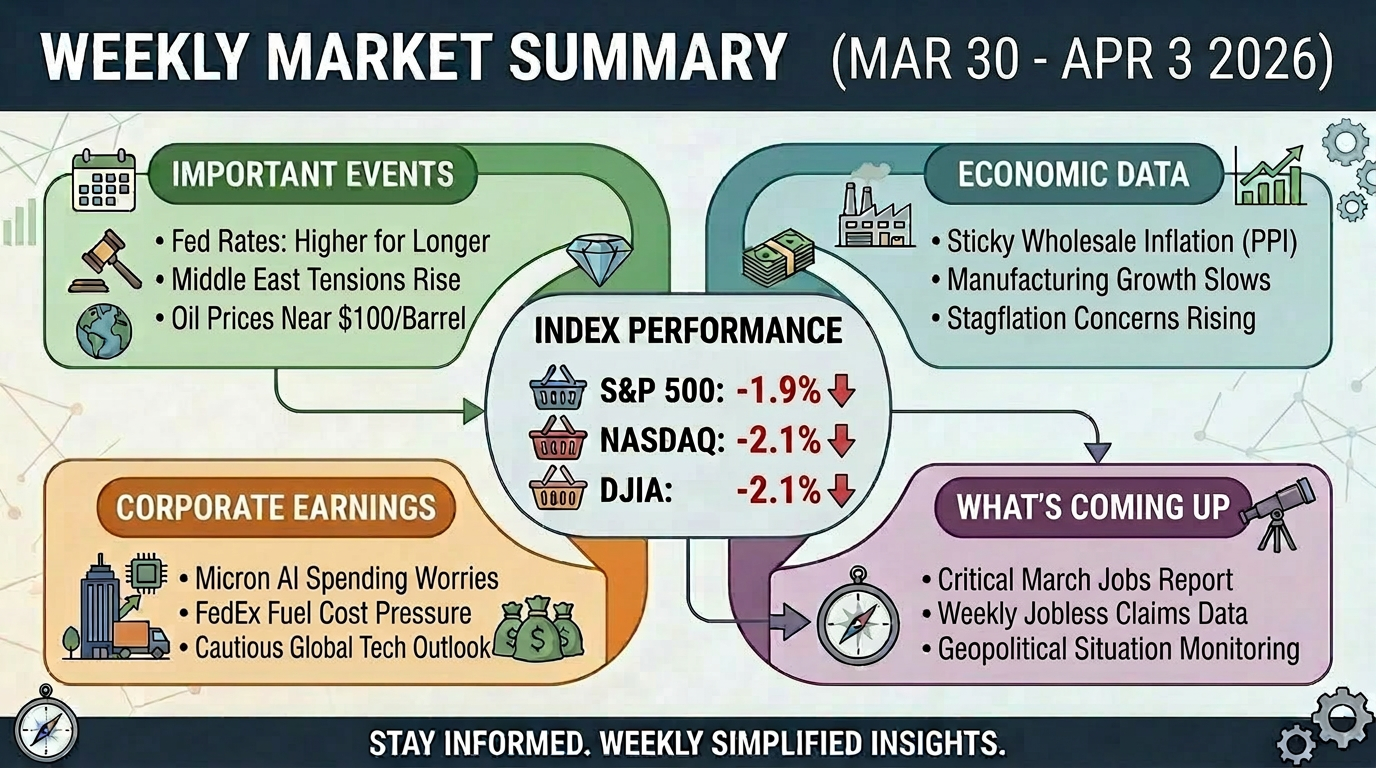

The major stock indexes have just concluded their fourth consecutive week of losses, marking one of the most difficult stretches for investors so far this year. Over the last five sessions (days), the S&P 500 retreated by 1.9%, while both the Nasdaq Composite and the Dow Jones Industrial Average dropped by 2.1%. This downward trend has pulled the markets deeper into negative territory for 2026; as of today, the S&P 500 is down 8.5% for the year, with the Nasdaq and Dow trailing at losses of 11.3% and 8.8% respectively. This week’s decline reflects a growing realization among investors that the path toward lower interest rates and stable inflation is proving to be much bumpier than originally hoped.

Important Events

The primary catalyst for this week’s sell-off was a significant shift in expectations regarding the Federal Reserve and the rising cost of energy. On Wednesday, several Federal Reserve officials delivered speeches making it clear that they are in no rush to lower interest rates. While investors began the year hoping for multiple rate cuts, the consensus this week shifted toward perhaps only one cut—or potentially none at all—in 2026. This "higher-for-longer" stance is a headwind for stocks because higher interest rates increase the cost of borrowing for both businesses and consumers, which reduces corporate profits and dampens overall spending. Simultaneously, geopolitical tensions in the Middle East intensified, pushing crude oil prices toward the $100-per-barrel mark. This spike in energy costs is a major concern because it fuels inflation, which in turn gives the Federal Reserve even more reason to keep interest rates elevated to prevent the economy from overheating.

Economic Data

The economic reports released this week painted a picture of "sticky" inflation that refused to cool down as quickly as forecasted. The most critical data point was the Producer Price Index (PPI), which measures inflation at the wholesale level, or the prices businesses pay each other for goods and services. The PPI rose 0.7% for the month, coming in higher than economists expected and suggesting that price pressures are still bubbling under the surface. Additionally, private payroll data indicated that while hiring remains steady, the pace of growth is beginning to slow in the manufacturing sector. This creates a challenging environment known as "stagflation," where economic growth begins to stall but prices remain high, leaving the Federal Reserve with very few easy options to support the market without risking further inflation.

Corporate Earnings

While the official first-quarter earnings season is still a week away, several early updates from global market leaders influenced investor sentiment this week. Micron Technology provided an update on its artificial intelligence (AI) initiatives; while demand for its chips remains at record highs, the company warned that the massive costs of expanding production are weighing on its short-term cash flow. In the logistics sector, FedEx faced selling pressure as investors reacted to the rising cost of jet fuel and diesel resulting from the surge in oil prices. Meanwhile, overseas, results from Chinese giants Alibaba and Tencent pointed to a cautious spending environment in Asia, adding to a global "risk-off" mood where investors preferred safer assets over stocks. For most of the week, these individual company stories were secondary to the broader anxieties regarding the global economy and the threat of regional conflict.

What’s Coming Up Next Week

Looking ahead to next week, the market will be hyper-focused on whether this losing streak can finally be broken. The most critical event will be the release of the March Jobs Report on Friday, which will show exactly how many positions the U.S. economy added and whether the unemployment rate is beginning to rise. Before that, investors will monitor weekly jobless claims on Thursday and manufacturing data to see if the high interest rate environment is causing the economy to shrink. Beyond the data, the focus will remain heavily on the situation in the Middle East. Any signs of a ceasefire or cooling tensions could lead to a sharp drop in oil prices and a "relief rally" for stocks. However, if tensions escalate over the weekend, we could see oil break firmly above $100, which would likely lead to further losses when trading resumes on Monday morning.