The Federal Reserve, The Bank of Banks

If you watch the evening news, you have likely heard reporters mention "The Fed" with a tone of serious importance. You might hear that they are having a meeting, making a major announcement, or deciding to raise or lower "rates." Despite how often this institution is talked about, very few people understand what it actually does.

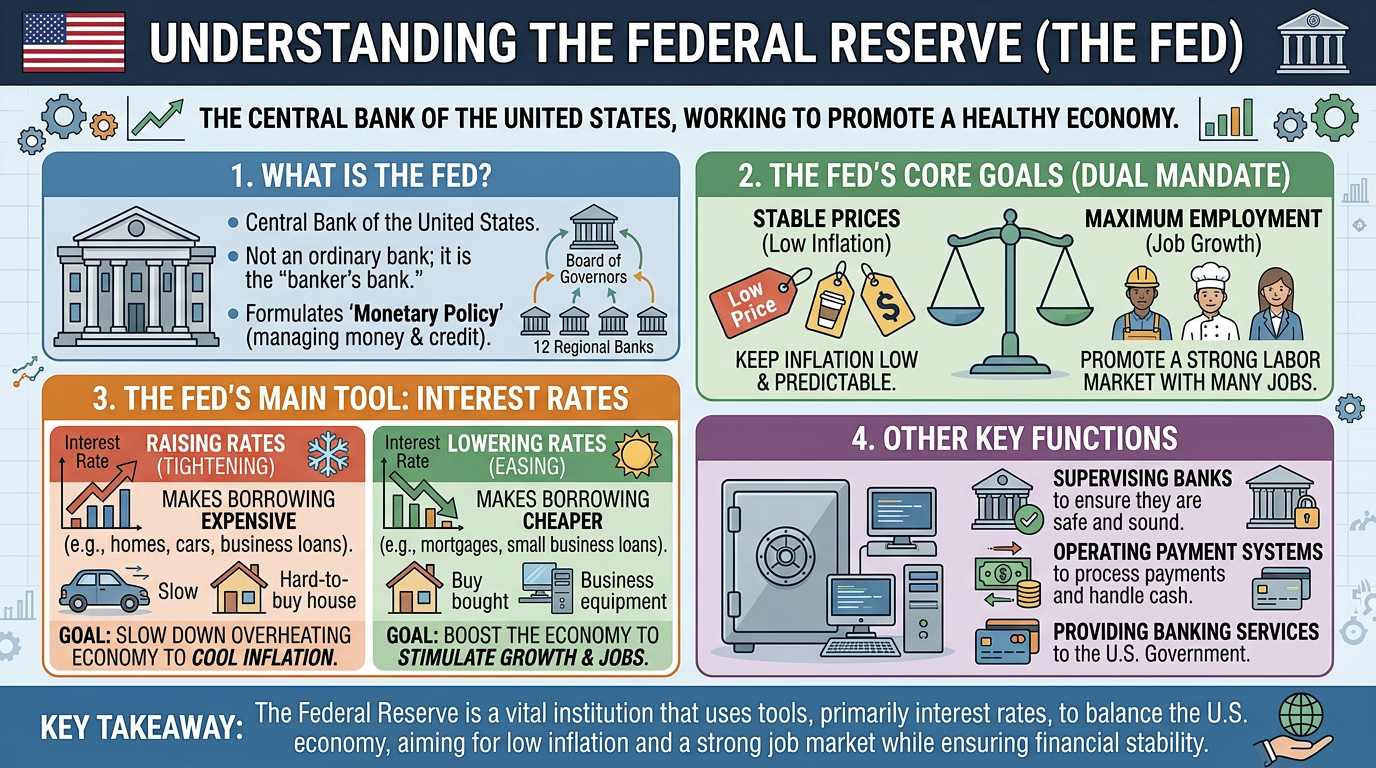

In simple terms, the Federal Reserve is the central bank of the United States. However, it is not a bank where you can open a checking account or deposit your paycheck. Instead, you can think of it as the "bank for banks," or the master control room for the entire country's financial system. Its primary job is to keep the American economy running as smoothly and stably as possible.

The Ultimate Balancing Act

To understand what the Federal Reserve does, it is helpful to know its two main goals, which economists officially call its dual mandate. Through this mandate, the government has tasked the Fed with a very specific, and often difficult, balancing act: keeping as many people employed as possible (maximum employment), while also keeping prices steady and predictable (minimizing inflation).

As we have explored with the job market and inflation, these two goals constantly pull against each other. If the economy is growing too fast and everyone has a job, people have a lot of money to spend. This high demand causes businesses to raise their prices, leading to inflation. On the other hand, if people stop spending money, businesses lose profit and are forced to lay off workers, causing unemployment to rise.

The Federal Reserve acts as the referee in this endless tug-of-war. They monitor the economy constantly to make sure it does not get too hot (causing prices to skyrocket) or too cold (causing massive job losses).

The Master Tool: The Interest Rate Lever

Because the Federal Reserve cannot force businesses to hire people or legally tell a grocery store what to charge for a gallon of milk, they have to influence the economy indirectly. They do this primarily by using one incredibly powerful tool: adjusting the cost of borrowing money, officially known as the federal funds rate (the rate at which the Federal Reserve lends to other banks, which, in turn, affects you).

Think of the economy like a car. The Federal Reserve uses interest rates as the gas pedal and the brakes.

When the economy is slowing down and people are losing their jobs, the Fed wants to step on the gas. They do this by lowering interest rates, which makes borrowing money very cheap. When borrowing is cheap, businesses take out loans to build new factories and hire more workers. Everyday people take out mortgages to buy homes or loans to buy cars. All of this borrowed money flows into the economy, creating jobs and driving growth.

However, if the economy is moving too fast and prices are rising out of control, the Fed has to hit the brakes. They do this by raising interest rates, making it much more expensive to borrow money. When loans are expensive, businesses pause their expansion plans, and people decide to wait before buying a new house or putting a big purchase on a credit card. Because everyone is spending less, businesses have to stop raising their prices to attract cautious buyers, which cools down inflation.

The Bank for Banks and You

You might wonder how a decision made by government officials in Washington directly affects your wallet. The connection lies in how your personal bank operates.

When the Federal Reserve decides to make borrowing more expensive, they are actually raising the rate they charge major banks to borrow money. To cover this higher cost, your local bank instantly raises the rates they charge you. This is why, within days of a Federal Reserve announcement, you will see the interest rates on new credit cards, auto loans, and home mortgages go up or down.

While the Fed does not set your personal credit card limit or approve your mortgage, they completely control the financial environment in which those decisions are made. They set the baseline cost of money for the entire country.

Summary

The Federal Reserve is the invisible hand guiding the national economy. By carefully monitoring the balance between the job market and the cost of living, they use the cost of borrowing money to keep the country financially stable. While their work can seem incredibly complex, their ultimate goal is deeply connected to your everyday life: ensuring that you have the opportunity to find a job, and ensuring that the money you earn retains its value when you go to the store.