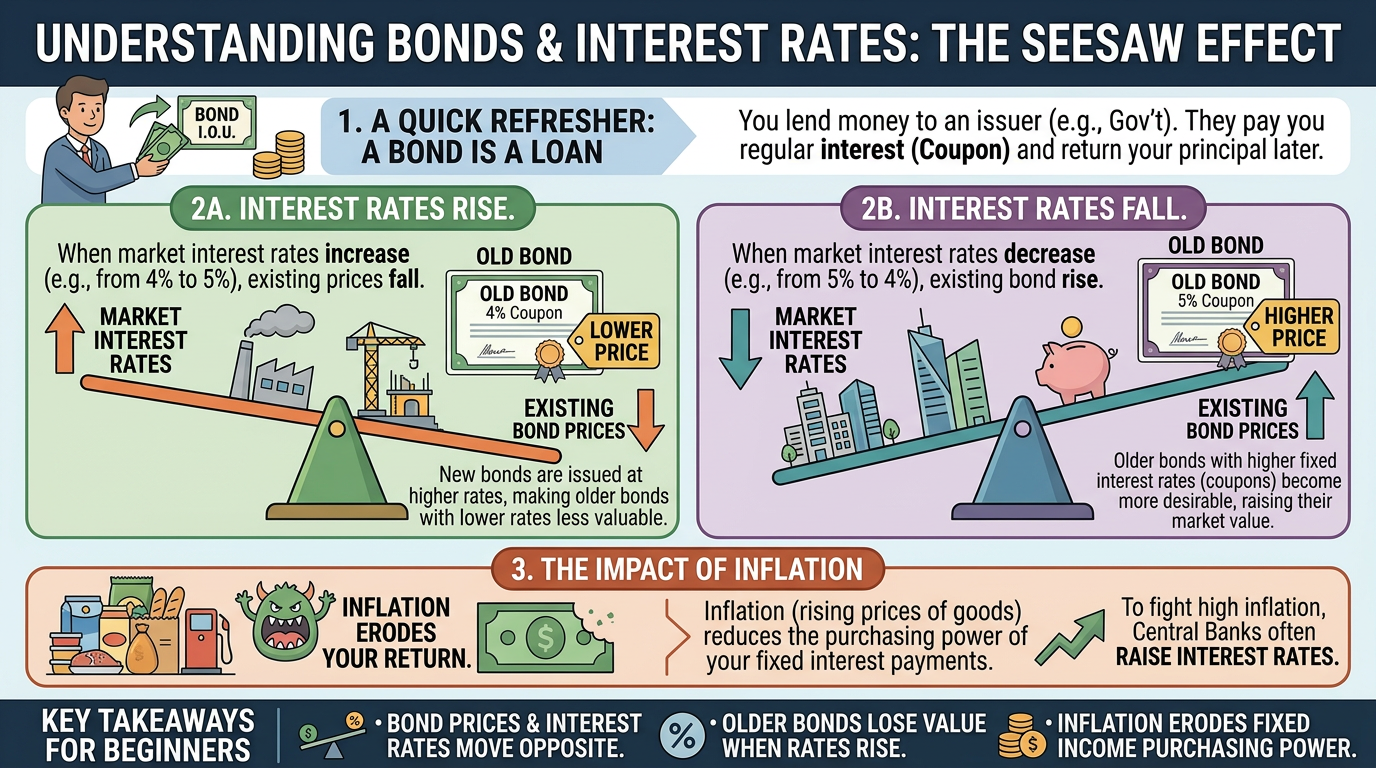

The Connection Between Bonds, Interest Rates, and Inflation

When you buy a bond or a U.S. Treasury, you are lending money in exchange for a fixed interest payment (and obviously the initial money back). But once you own that bond, its value in the real world does not exist in a vacuum. It is constantly influenced by two massive economic forces: interest rates and inflation. Understanding how these forces interact with your fixed-income investments is crucial for protecting your wealth, especially when the broader economy is going through periods of rapid change.

The Seesaw Effect: Bonds and Interest Rates

The relationship between bond prices and interest rates is one of the most fundamental rules of investing. They move in opposite directions, exactly like a seesaw. If interest rates in the broader economy go up, the value of the bonds you already own goes down. If interest rates fall, the value of your existing bonds goes up.

To understand why this happens, imagine you buy a Treasury bond that pays 3% interest. A year later, the economy changes, and the government starts issuing brand new Treasury bonds that pay 5% interest. If you want to sell your older, 3% bond to another investor, nobody will pay full price for it because they could simply buy a new one paying 5%. To convince someone to buy your old bond, you have to sell it at a discount. Conversely, if new bonds are only paying 1%, your 3% bond suddenly becomes highly valuable, and you can sell it for a premium (higher price). This is why a bond's market price constantly fluctuates even if the issuer is perfectly safe.

The Silent Thief: Inflation's Impact on Bonds

While interest rates directly affect the trading price of your bond, inflation affects the actual purchasing power of the money your bond generates. Inflation is the general increase in the prices of goods and services over time. Because regular bonds pay a fixed amount of interest, inflation acts like a silent thief. If your bond pays you a fixed $50 a year, but the cost of groceries and gas doubles, that $50 buys you much less than it used to.

To figure out if your bond is actually making you wealthier, you have to calculate your "real yield." This is simply your bond's interest rate minus the current rate of inflation. If your bond pays 4% interest, but inflation is running at 6%, your real yield is actually -2%. Even though you are technically making money on paper and your account balance is going up, you are quietly losing purchasing power (the amount you can actually buy with your money) in the real economy.

The Federal Reserve: Connecting the Dots

Inflation and interest rates do not just move randomly; they are deeply connected through the actions of central banks, like the Federal Reserve in the United States. When inflation gets too high and the cost of living starts climbing out of control, the Federal Reserve steps in to cool the economy down by intentionally raising interest rates. This makes borrowing money more expensive for businesses and consumers, which slows down spending and eventually lowers prices.

However, as we learned from the seesaw effect, when the Federal Reserve raises those interest rates to fight inflation, the market prices of existing bonds drop. This creates a challenging environment for bondholders, who face both dropping bond values and the eroding power of inflation simultaneously. It is a classic economic cycle that all fixed-income investors have to navigate.

Shielding Your Portfolio with TIPS

Fortunately, the government created a specific type of Treasury bond designed to protect investors from these exact economic forces, known as Treasury Inflation-Protected Securities, or TIPS. With a regular bond, the original amount of money you invest stays exactly the same forever, no matter what happens in the economy. A TIPS bond is uniquely designed to protect you from rising prices. When the Consumer Price Index (the main measure of inflation) increases, the government automatically increases the core value of your TIPS bond to match it, ensuring your savings never lose their buying power.

If inflation goes up, the core value of your TIPS bond increases. Because your interest payments are calculated as a percentage of that core value, your interest payments get bigger, too. While TIPS usually offer a lower starting interest rate than regular Treasuries, they act as an insurance policy. By incorporating them into your portfolio, you ensure that at least a portion of your savings will maintain its true purchasing power, no matter what inflation or interest rates do to the broader economy.

Summary

In short, the value and earning power of your bonds are constantly shaped by interest rates and inflation. Bond prices and interest rates move in opposite directions, when market rates go up, the trading price of your existing bonds goes down. Meanwhile, inflation acts as a silent thief, eroding the real purchasing power of your fixed interest payments over time. Because the Federal Reserve often raises interest rates to fight high inflation, traditional bondholders can face dropping bond values and decreasing purchasing power simultaneously. However, investors can protect their portfolios by utilizing specialized tools like Treasury Inflation-Protected Securities (TIPS), which automatically adjust their core value to keep pace with the rising cost of living and preserve your true wealth.